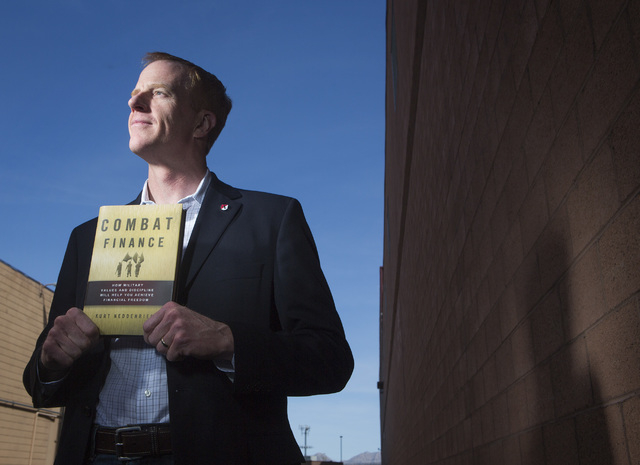

Retired soldier combines military, Wall Street experience in personal finance book

From basic training to the battlefield, Elko author Kurt Neddenriep offers his advice in “Combat Finance,” a new book for citizens and soldiers on how to achieve financial freedom and avoid becoming a “soup sandwich,” as his drill sergeant put it.

“Basically, like the drill sergeant said, a soup sandwich is soup between two slices of bread. It’s just a big ball of mush. You can’t eat that. It’s falling through your fingers. It doesn’t accomplish the goal,” he said.

“You’re going to go hungry. So if you want your finances in order, if you want to be that ham sandwich or that peanut butter and jelly sandwich, you want it to taste good and have it fulfill you,” Neddenriep, 43, said in a recent interview.

A retired lieutenant colonel with the Nevada Army National Guard, he has had a dual career from 1990 until he began a year-long project in February 2013 to write “Combat Finance.” The 202-page, hardcover book published by John Wiley &Sons Inc., hit bookstore shelves Jan. 28. It sells for $22.95. Neddenriep is donating one-third of his earnings from the book to financial education for military service members and their families.

His inspiration for “Combat Finance” came during the height of the Great Recession while he was deployed for Operation Enduring Freedom. In that period, the housing market collapse and unemployment hit Las Vegas hard.

“It was sort of like being on a sabbatical during one of the worst crises we’ve been through,” he said.

“The same soldiers that did so well in the military and that structured environment often times would walk out the front door and their financial lives were in shambles. You hate seeing your people suffer in any way, whether it’s physical or financially.”

At the time, he was the executive officer for the 221st Cavalry Regiment’s Wildhorse Squadron, which endured a combat deployment to Afghanistan that ended in 2010. In all, 730 troopers from 1st Squadron, 221st Cavalry went to Afghanistan. While overseas, they pulled 6,200 patrols to fight militants and escort convoys. Some soldiers built schools and hospitals in remote areas of the war-torn country.

In civilian life, with a degree in business administration from the University of Nevada, Reno, Neddenriep is a senior vice president for a major Wall Street firm.

He combined his military and business skills to advise clients and soldiers on how to achieve financial freedom. For the most part, his advice to them is not about having a bigger bank account than their neighbors or driving a fancier car.

“They want to not be a soup sandwich because they want to see their kids get through college,” he said. “They want to see their daughter have a beautiful wedding. They want to have a retirement where they can be comfortable and go spend time with their grandkids.

“It’s not usually about the money per se, but that being good stewards of your money allows those non-financial things, those non-financial goals in your life to be achieved.”

In the aftermath of the combat tour, he drew some conclusions that led to 10 principles for achieving financial freedom and getting the downtrodden on their feet.

“When we got back, I was able to see some people had made it through this downturn just fine. Others really took the brunt financially,” he said. “What were the common denominators of those people who made it through the downturn versus those who didn’t make it through well?”

What he discovered from hundreds of examples was that surviving the downturn was not so much related to a particular career field or income level. Rather it had to do with maintaining certain budget principles and being lucky enough to avoid a devastating financial blast, which he equates to staying to the left in time of an improvised explosive device, or IED.

“We were always talking about left of the blast. If we’re looking at a time continuum, you usually read left to right. Time is going on, your patrol is going down the road. Everything is going great. When the blast hits, there’s only certain things you can do at that point,” he said.

“You can provide security. You can render aid. You can call in medevac. You can do those kinds of things. But to the left of the blast there are lot more things you can do. You can send UAVs (Unmanned Aerial Vehicles) over the route to see if there is anything unusual. You can watch for kids and shopkeepers that are normally there that aren’t today. You can watch for people standing around paying particular interest to your patrol that usually aren’t there.

“Meaning, there are all kinds of actions we can take before the blast that will help us should the blast come or maybe even avoid the blast in the future, or avoid it all together,” he said.

One of the first points he makes in “Combat Finance” is “making sure you have an operational reserve that is one month’s worth of your needs budget and a strategic reserve that is at a minimum six months and at a maximum two years of your needs budget.”

Next, he said, is to make sure “that our home does not exceed 35 percent of our take-home pay. What your concern is as an individual investor should be, ‘Can I pay my home payment but also still have the money to go outside the wire to fight the financial fight I need to get my kids through college, to save for retirement and to do all those other things.’

“And if too much of your assets are going toward that home, that FOB (forward operating base) or COP (combat outpost) as I talk about in the book, you don’t have the manpower outside the wire to go win the war,” he said.

For those who have gotten hit by the financial blast through job loss or from paying on a home that costs more than its worth, there is some salvation for veterans by using government-backed loans from the Department of Veterans Affairs.

“First step. Build up our operating reserve. Second step, we build up our strategic reserve,” Neddenriep said. “While we’re building our strategic reserve it’s OK to do a simultaneous operation to get back into a home. And that’s where that VA loan could be a good choice because often times you don’t have to put any money down.

“Hopefully, over time, your home is going to be an appreciating asset. But the key thing is, it still has to meet that maximum 35 percent of your take-home pay,” he said. “That’s Kurt’s ‘Combat Finance’ rule because I want you to have a cushion to absorb one of the two people in your family losing their income or having a reduction in income.

“I want us to have what we call in the military, freedom of maneuver. We don’t want to be locked in a firefight that we can’t move an inch without getting shot by the enemy. We want to … have some ability to move and flex and adjust to attack the enemy. And that’s what keeping that house to 35 percent of our take-home income does.”

Contact Keith Rogers at krogers@reviewjournal.com or 702-383-0308. Find him on Twitter: @KeithRogers2.