Status check on national master-plan sales reveals slowing market

A routine check on national master-plan sales exposed a slowing new-homes market.

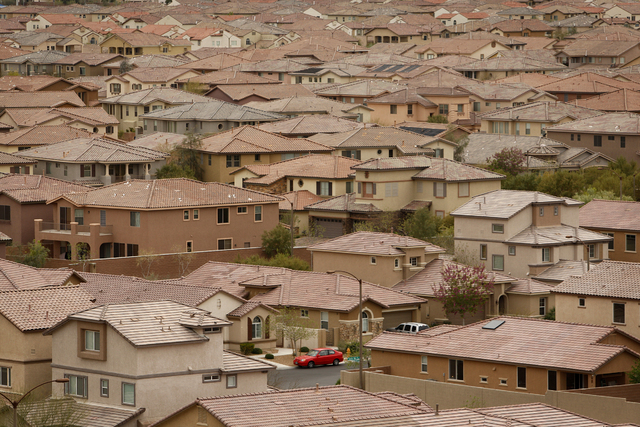

When Washington-based RCLCO put out its midyear update July 9 on planned-community sales, it showed a significant slump in closings among Southern Nevada’s best-sellers.

No need to panic yet: Communities across the country saw sales dip, with nine of RCLCO’s top 20 master plans experiencing drops in activity. Nor does the report herald another market crash, observers say.

What it does show is how the local market is still struggling to find a steady recovery pace amid waning investor interest and flagging land supplies.

Here’s how the market looked at the end of June: Mountain’s Edge, in the southwest valley, ranked No. 5 in the nation for closings, with 341 sales through the first half of 2014. That was a 19 percent drop from mid-2013. At that pace, Mountain’s Edge is on track to close about 680 units this year, down from 841 sales in 2013.

The northwest’s Providence placed No. 8, with 282 sales by the end of June. That was down 22 percent from a year earlier. And Summerlin ranked No. 13, its 248 closings a 12 percent falloff from a year earlier.

So what’s going on?

Well, for starters, investors have backed off as improving prices have hurt potential returns, said Dennis Smith, president and CEO of Home Builders Research in Las Vegas.

At the same time, while the local economy is better than it was in the downturn, it’s not completely recovered, Smith said. The city still hasn’t restored the jobs it lost in the recession, and median resale prices, despite surging in the past 18 months, remain a good third below their 2006 peak. That means local consumers aren’t doing quite well enough yet to pick up the slack as investors stopped buying.

It’s not just master plans feeling the slowdown. Sales among all local new-home subdivisions were down 22.6 percent year over year from January through April, according to local research firm SalesTraq. Resales slumped as well, dropping 13 percent in the first six months of the year, the Greater Las Vegas Association of Realtors reported July 7.

And for what it’s worth, even the nation’s best-selling master plan took a dive: The Villages in Ocala, Fla., closed on 1,455 units, down 15 percent year over year.

“The (Las Vegas) market is not in any type of boom state, and it’s not in a distress state,” Smith said. “It’s just kind of slogging along. It looks like it’s going to stay that way until we see the overall local and national economies get stronger. I think the level of production we’re at is probably where we’re going to be for at least a couple of years.”

■ California investors are buying local apartment complexes.

Brokers with Marcus &Millichap closed on the $7.7 million sale of Casa Del Sol, a 148-unit, Class C multifamily neighborhood at 5100 O’Bannon Drive. Perry White, vice president of investments, and Brett Beck, an investment specialist, represented the seller, Central Park Apartments LLC.

The buyer was FPA 4 Casa Del Sol LLC, which the Clark County assessor’s office lists as a Newport Beach, Calif.-based group.

Casa Del Sol was built in 1977.

■ An Internet entrepreneur made a large commercial play with the help of brokers from CBRE.

Daniel Negari dropped $4.8 million to buy Tropicana Executive Center, a 15-building office park at 1455 and 1515 E. Tropicana Ave. The complex, on 8.5 acres, includes 101,311 square feet of space.

Marlene Fujita Winkel of CBRE represented Negari in the deal.

CBRE’s Charles Moore worked with Fujita Winkel to represent the seller, Jefferson Pilot Investments.

Negari said he will refurbish Tropicana Executive Center and bring in new tenants.

In October, Negari bought for $1.1 million a 0.76-acre commercial property at 2121 E. Tropicana Ave. to serve as a hub for his Internet businesses.

■ Brokers with Voit Real Estate Services have completed three sizable lease deals.

Robin Civish and Lauren Tabeek represented landlord Alisiam Ren III LLC in its 60-month lease of 3,542 square feet of office space at 3330 E. Flamingo Road, inside the Renaissance III Shopping Center. Mary McClellan of Berkshire Hathaway HomeServices represented the tenant, Las Vegas Urban League, in the $304,164 deal.

Kevin Higgins, Garrett Toft and Zac Zaher represented tenant Sunbay Supplies LLC in a 38-month lease renewal on 15,520 square feet of industrial space at 4701 Cameron St. The transaction was valued at $287,825.

Higgins, Toft and Zaher also represented landlord Hughes Airport Realty Owner LLC in a 65-month lease of 5,555 square feet of industrial space at 731 Pilot Road to tenant Schneider Electric Buildings Americas. Tyler Ecklund of CBRE assisted the tenant in the $261,584 agreement.

Jayne Cayton and Matthew Kreft helped arrange an 89-month lease on 1,457 square feet of office space at 1701 W. Charleston Blvd., inside the Charleston Tower. Cayton and Kreft represented landlord Charleston Holdings LLC in the $203,033 deal, while US National Commercial Real Estate represented tenant Dr. Michael J. Daccache Oral &Maxillofacial Surgery Ltd.

■ The Southern Nevada Association of Home Builders has put together a panel of some of the city’s biggest builders to discuss development.

Top local executives with Beazer Homes, Lennar and American West Development will appear on a panel at the association’s membership meeting at 7:30 a.m. Aug. 14 inside Cili at the Bali Hai Golf Club, at 5160 Las Vegas Blvd. South. The cost to attend is $25. For more information, call 702-794-0117 or visit snhba.com.

Contact reporter Jennifer Robison at jrobison@reviewjournal.com. Follow @J_Robison1 on Twitter.