Las Vegas’ housing market hit the brakes in ‘22 — don’t expect it to speed up in ‘23

Las Vegas’ housing market is ending this year drenched in cold water, following a red-hot 2021.

A sharp jump in mortgage rates sparked big drops in home sales, widespread price cuts, huge increases in available inventory and more incentives from builders. Housing markets across the United States also slowed, but Las Vegas retreated faster than the nation overall in key ways.

With 2023 around the corner, Southern Nevada’s market remains in something of a logjam, and industry experts predict a muted year ahead for housing nationwide.

Prospective buyers have been sidelined amid big jumps in monthly payments, and would-be sellers have had incentives to stay put, as they likely have a lower mortgage rate on their current home than what they’d get on a new purchase.

Nicole Bachaud, senior economist with listing site Zillow, told the Review-Journal that mortgage rates will likely stabilize next year.

But she expects home sales nationwide to remain “far lower” than in 2021 and 2020, when markets around the U.S., including in Las Vegas, heated up.

“We’re definitely expecting things to be cooled and slow compared to what we saw the past couple of years,” she said.

Taylor Marr, deputy chief economist with brokerage firm Redfin, recently predicted that U.S. resales will tumble by about 16 percent next year, and the median sales price for a home will slide by roughly 4 percent.

He told the Review-Journal that 2022 marked one of the biggest “U-turns” for the housing market and noted that mortgage rates climbed at the fastest pace ever.

“It caused the party to end,” he said.

‘Sharp’ pullback

Las Vegas’ housing market was still heated at the beginning of 2022. Sellers were fielding a “frenzy” of offers, and buyers were bidding over asking prices and waiving contingencies, said Brandon Roberts, president of trade association Las Vegas Realtors.

But with Americans paying higher prices for gasoline, groceries and other goods, the Federal Reserve started raising interest rates in an effort to fight inflation. This caused borrowing costs for mortgage loans to jump sharply.

By late October, the average rate on a 30-year home loan was 7.08 percent, up more than double from a year earlier to the highest rate in two decades.

Roberts, a broker with Signature Real Estate Group, expected Las Vegas’ market to slow. But he didn’t think the pullback would happen as “fast” and “sharp” as it did.

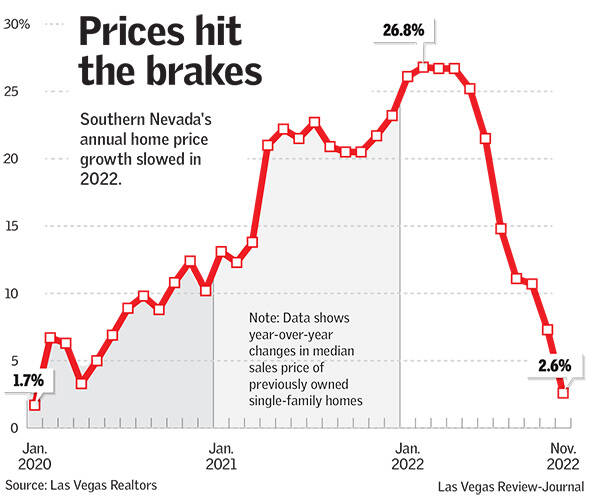

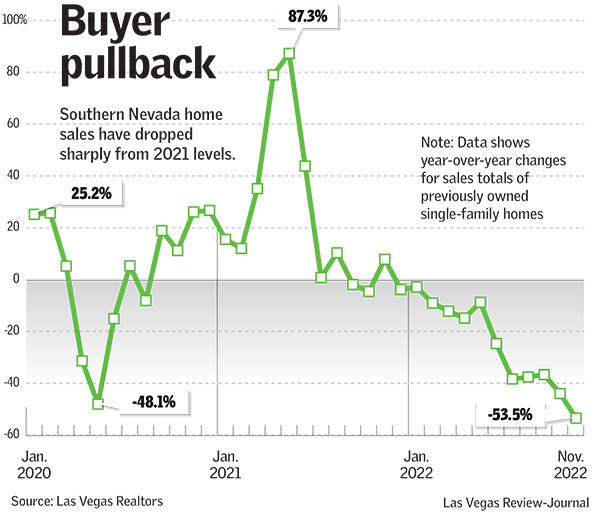

On the resale side, 1,521 houses traded hands in November, down 53.5 percent from the same month last year, while 7,342 houses were on the market without offers at the end of November, up 161.7 percent from a year earlier, Las Vegas Realtors reported.

Single-family homes sold for a median price of $430,990 in November, the lowest level of the year, and down from a record-high of $482,000 in May, according to association data.

‘Shift in mindset’

Southern Nevada homebuilders have also seen sharp drops in sales this year. Amid the market slowdown, they have offered more incentives to buyers and higher commissions to agents who bring them in, real estate sources have said.

Builders logged 350 net home sales — newly signed purchase contracts minus cancellations — in Southern Nevada in October, down 59 percent from the same month last year, according to Las Vegas-based Home Builders Research.

Builders also pulled 545 new-home permits in October, down 55 percent year-over-year, indicating a sharp drop in construction plans, and their land buying was “basically non-existent,” wrote Andrew Smith, the research firm’s president.

Smith said in an interview that Las Vegas’ homebuilding market took a “fast turn the other way” as soon as mortgage rates climbed.

He said rates were expected to rise, but ultimately, the pace of the hikes “hit people pretty hard.”

Mortgage rates have ticked lower in recent weeks but are still more than double what they were late last year. As of last week, the average rate on a 30-year home loan was 6.27 percent, up from 3.05 percent a year earlier, mortgage buyer Freddie Mac reported.

Smith doesn’t expect many new subdivisions to open in Southern Nevada next year, and he doesn’t think home prices will “fall off the cliff by any means,” figuring they may even tick higher.

Still, he’s waiting to see a “shift in mindset,” as people need to “accept” that mortgage rates won’t drop back to 3 percent anytime soon, he said.

‘Jarring’ transition

Fueled by record-low mortgage rates that let buyers stretch their budgets, and more out-of-state buyers than usual, Las Vegas’ housing market accelerated to its most frenzied pace in years in 2021.

Homes sold rapidly, prices hit all-time highs practically every month, buyers showered properties with offers and builders regularly raised prices and put house hunters on waiting lists.

Las Vegas’ housing market has a track record of speeding up then hitting the brakes. And lately, it has “cooled down much faster than the rest of the country,” Redfin’s Marr said.

Southern Nevada house prices slid 2.4 percent from August to September, compared with a 1 percent dip nationwide in that time, according to the S&P CoreLogic Case-Shiller index.

A higher share of sellers have cut their prices, as 42 percent of Las Vegas-area home listings had a price drop in September, compared with 27.5 percent nationally for the same period, Zillow reported. Both figures were up from the 9 percent-range in February.

Sales volume has also shrunk faster here. Among the 50 most populous metro areas in the nation, pending sales dropped the most in Las Vegas, falling 65 percent year-over-year in the four weeks ending Nov. 27, Redfin reported.

Bachaud, of Zillow, said she wasn’t surprised housing nationally hit the brakes, as it’s moving toward a “more normal, healthy, balanced market.”

But, she said, it’s still “far off from that” — and the transition to get there is “going to feel really, really jarring.”

Contact Eli Segall at esegall@reviewjournal.com or 702-383-0342. Follow @eli_segall on Twitter.